Federal Agency/Employee Educational Solutions

Medicare Question Federal Retirees Should Not Ignore

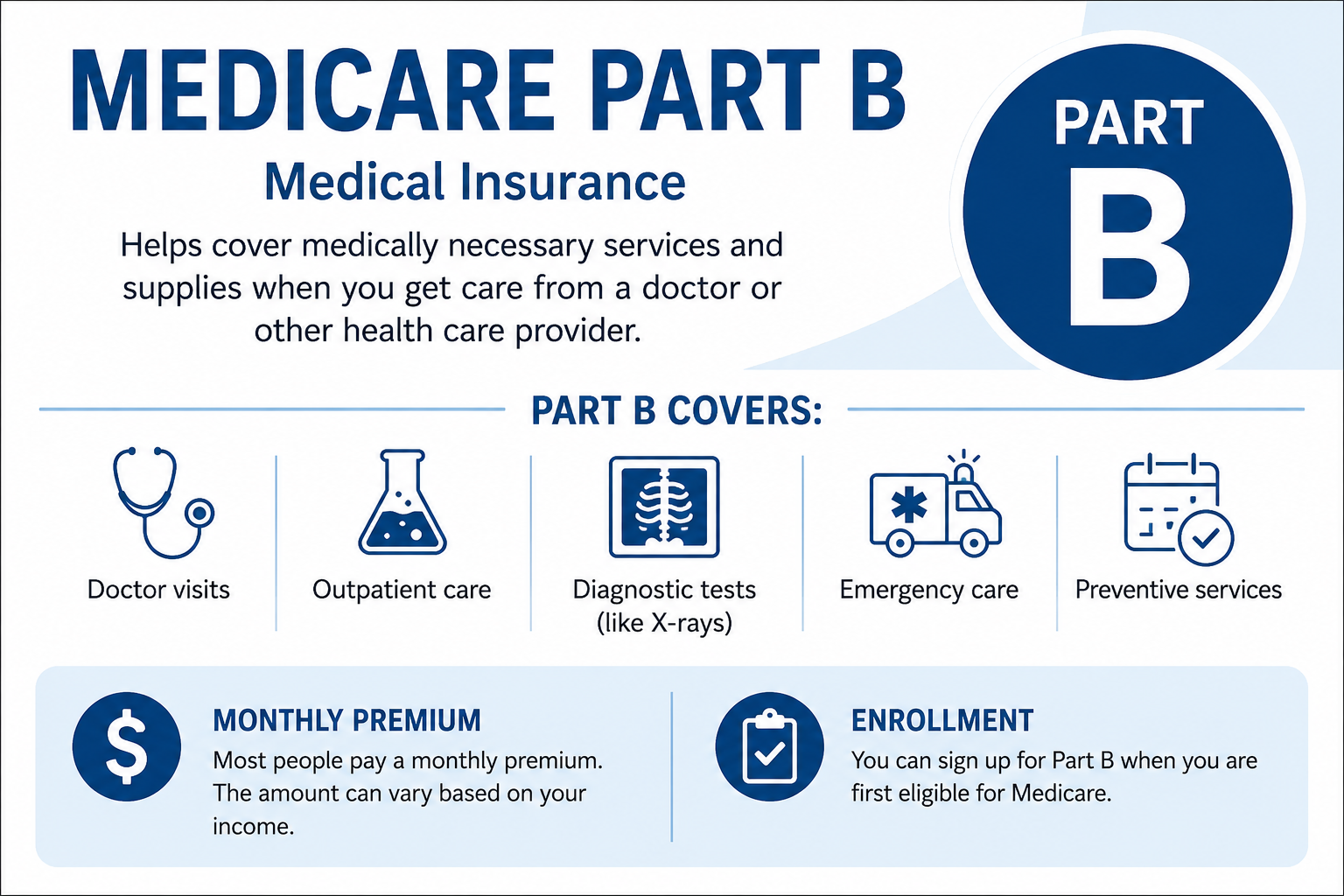

Federal retirees should not ignore the rising‑stakes question of whether to enroll in Medicare Part B — because premiums, penalties, and FEHB coordination rules are changing in ways that can significantly affect lifetime healthcare costs.

The Core Issue

The 2026 Medicare Trustees Report shows that Part B premiums are climbing, and the decision to enroll — or not — now has larger financial consequences for federal retirees who keep FEHB in retirement.

For most federal retirees, the question is not “FEHB or Medicare?” It’s whether adding Medicare Part B to FEHB is worth the extra premium — and what happens if you delay.

Why This Question Matters Now

1. Part B premiums are rising

Standard Part B premium in 2026 is $202.90/month.

Higher‑income retirees face IRMAA surcharges starting at $109,000 (single) or $218,000 (joint) MAGI.

These surcharges can add hundreds per month.

2. Delaying Part B can trigger a permanent penalty

10% added to your Part B premium for every 12 months you delay past eligibility.

This penalty lasts for life.

3. FEHB + Medicare often eliminates out‑of‑pocket costs

Many FEHB plans waive deductibles, copays, and coinsurance when Medicare is primary. This can mean:

Lower total medical spending

Predictable costs

Better protection from large claims

4. You are not required to enroll in Part B to keep FEHB

This is where many retirees get confused.

You can keep FEHB for life without Part B.

But skipping Part B means FEHB stays primary — and you keep paying FEHB cost‑sharing.

5. Postal retirees face different rules

Under the new PSHB program, most postal retirees must enroll in Part B to keep coverage.

The Real Question Federal Retirees Must Answer

Does the added cost of Medicare Part B provide enough value — in reduced FEHB cost‑sharing and improved coverage — to justify the premium and avoid penalties?

For many retirees, the answer is yes, especially if:

You expect moderate or high medical usage

Your FEHB plan waives cost‑sharing with Medicare

You want predictable, low out‑of‑pocket costs

You want to avoid lifetime penalties

For others — especially very healthy retirees or those with tight budgets — the answer may differ.

Federal retirees can’t ignore the Medicare Part B decision because rising premiums, lifetime penalties for delaying, and FEHB coordination rules make this one of the most financially consequential choices they will face in retirement.

Sources:

Government Executive

Senior Health Times

Prior Federal Service May Significantly Change Both Your Eligibility for a FERS Retirement and Your Annuity Amount

The key is understanding which types of service count toward eligibility, which count toward computation, and how refunds or breaks in service affect both.

1. Creditable Service Basics

Under FERS, your retirement is based on:

Creditable civilian service (with retirement deductions withheld)

Potentially creditable military service (with deposit)

Whether any refunded service has been repaid (redeposit)

OPM’s FERS Creditable Service rules determine what counts toward eligibility and annuity computation.

🟦 A. If You Leave Federal Service and Return Later (Break in Service)

1. Your prior service still counts toward eligibility

Even if you leave federal service for years, your earlier FERS-covered service generally still counts toward:

Meeting the Minimum Retirement Age (MRA) + service requirements

Deferred retirement eligibility (if you have ≥5 years of creditable service)

OPM confirms that former employees with ≥5 years of service may claim a deferred retirement at age 62 or MRA+10.

2. Your annuity computation depends on whether you took a refund

If you did not take a refund → Your prior service counts fully toward both eligibility and computation.

If you did take a refund → See Section C below.

🟦 B. If Your Federal Service Was Interrupted (Breaks but No Refund)

If you leave federal service but leave your retirement contributions in the system, then:

All prior service remains fully creditable

You retain eligibility for deferred retirement if you never return

If you return, your service is treated as continuous for retirement purposes

This is the simplest scenario—no redeposit needed.

🟦 C. If You Took a Refund of FERS Contributions

This is the most misunderstood area.

1. Taking a refund voids your annuity rights for that period

OPM states clearly:

“Receiving a refund of retirement deductions voids all annuity rights under FERS.”

2. But you can restore that service if you return to federal employment

Thanks to Public Law 111‑84 (2009), employees covered by FERS on or after Oct. 28, 2009 may make a redeposit to restore refunded service.

3. What happens if you do NOT redeposit?

If you return to federal service but do not repay the refund:

The refunded service counts toward eligibility

The refunded service does NOT count toward annuity computation

Your annuity will be smaller, and survivor benefits based on that service will also be reduced

4. What happens if you DO redeposit?

The refunded service is fully restored for both eligibility and computation

You must repay the refund amount + interest

🟦 D. If You Had CSRS Service Before FERS

If you transferred from CSRS to FERS:

A refund application can return both CSRS and FERS deductions

CSRS redeposits have always been allowed

You may request only the CSRS portion be refunded

This matters because CSRS redeposits can restore valuable pre‑1987 service.

🟦 E. Deferred Retirement (If You Leave and Never Return)

If you leave federal service with ≥5 years of creditable service and do not take a refund:

You may claim a deferred FERS annuity at:

Age 62 with ≥5 years

MRA+10 with ≥10 years (reduced benefit unless postponed)

OPM confirms this option for former employees.

🟦 F. Key Takeaways

1. Breaks in service do NOT erase your retirement credit.

Your service remains on record unless you take a refund.

2. Refunds are the biggest risk to your retirement value.

A refund:

Eliminates annuity rights for that period

Can be reversed only by redeposit (with interest)

3. Even refunded service still helps you meet eligibility rules.

It counts toward:

MRA+10

20‑year or 30‑year thresholds

Deferred retirement eligibility

4. Redeeming refunded service can significantly increase your annuity.

Especially for employees with long early‑career service.

Sources:

OPM – FERS Refund Fact Sheet

OPM – Types of retirement

OPM – FERS Creditable Service Rules

OPM Addresses Worries Regarding Plan to Access FEHB/PSHB Medical Records

OPM moved to calm growing privacy concerns after proposing to access detailed FEHB and PSHB medical claims data—including office visits, treatments, and prescriptions—to improve program oversight. Critics, including NARFE, AFGE, and more than a dozen Democratic lawmakers, warned the plan lacked clarity on why OPM needs such data, how it would be protected, and whether it could expose sensitive information or violate privacy laws.

In response, OPM Director Scott Kupor said the data would be de‑identified before OPM receives it, with names, Social Security numbers, addresses, and other PII removed. Only ZIP code, year of birth, and member ID (which OPM will replace with random identifiers) would remain. Kupor emphasized that the data would be encrypted, stored separately, and used to detect fraud and improper billing in real time—something OPM currently can only do after the fact through IG audits.

Sources:

FEDweek

SouthworthPCSee less

OPM Expands US Tech Force With New Industry Partnerships

The US Office of Personnel Management (OPM) today announced additional leading technology companies have committed to partnering with the US Tech Force (Tech Force), the government-wide initiative to recruit top technologists to modernize the federal government and strengthen America’s technical workforce.

Follow link to read more from the OPM: https://www.opm.gov/.../opm-expands-us-tech-force-with.../

Disclaimers Are Used Progressively More in Federal Employee Estate Plans

A disclaimer allows a beneficiary to refuse an inheritance, causing the asset to pass directly to the next designated beneficiary as if the original beneficiary had never received it.

Federal employees often have complex estates that include retirement benefits, Thrift Savings Plan (TSP) accounts, life insurance, and other beneficiary-designated assets. As a result, estate planners are increasingly incorporating disclaimers to provide flexibility after death.

Key reasons include:

Flexibility: Beneficiaries can decide after death whether accepting an asset is the best choice based on current circumstances.

Tax planning: Disclaimers can help reduce future estate taxes and facilitate more efficient wealth transfers.

Changing family needs: They can address unexpected situations such as divorce, creditor issues, special-needs concerns, or changes in financial circumstances.

Adapting to outdated plans: Disclaimers provide a way to adjust distributions when laws, assets, or family dynamics have changed since the estate plan was created.

For federal employees, disclaimers are particularly valuable because they help coordinate the transfer of multiple benefits and accounts while preserving flexibility for beneficiaries.

Sources:

Journal of Accountancy

VCLaw.com

Knoxlaw

Legal Information Institute/Cornell University

Combining Retirement Accounts and Roth Conversions: Today’s Slott Report Mailbag

Question:

I have a new client who has an old SEP IRA as well as a traditional IRA with funds that were rolled over from his 401(k) plan. Can we combine these two accounts?

Answer:

Yes. These accounts can be combined. A SEP IRA is really just the same as a traditional IRA once the contributions are made. There is no reason to keep these accounts separate.

Question:

I am working with a couple on possible Roth conversions and retirement distribution planning. The husband inherited an IRA from his mother. If the husband passes and the wife inherits this inherited IRA, what are the options available to the surviving spouse on this inherited IRA? Can she do a Roth conversion?

Thanks,

Rick

Answer:

Hi Rick,

A Roth conversion would not be possible in this situation. The IRA was originally inherited by the husband from his mother. The husband is a non-spouse beneficiary, and non-spouse beneficiaries cannot convert inherited IRAs. If the wife inherits this IRA as a successor beneficiary, she would be a non-spouse beneficiary as well because she was not married to the original IRA owner (her husband’s mother). That means conversion is not allowed.

Copyright © 2026, Ed Slott and Company, LLC Reprinted from The Slott Report, 5/28/26 with permission. Combining Retirement Accounts and Roth Conversions: Today's Slott Report Mailbag - Ed Slott and Company, LLC. Ed Slott and Company, LLC takes no responsibility for the current accuracy of this article.

Our first priority is helping you take care of yourself and your family. We want to learn more about your personal situation, identify your dreams and goals, and understand your tolerance for risk. Long-term relationships that encourage open and honest communication have been the cornerstone of my foundation of success.

2026 TSP Diversification Guide

This comprehensive guide explains the January 1, 2026, changes to TSP catch-up contributions, in-plan Roth conversions, and updated contribution limits — and outlines how federal workers can use rollover provisions to diversify beyond the TSP's five core funds

WOODLAND HILLS, Calif., May 25, 2026 /PRNewswire/ -- American Alternative Assets, a BBB A+ rated precious metals dealer, today released a free, comprehensive 2026 TSP Diversification Guide to help federal employees, retirees, and uniformed employees service members navigate a slate of significant Thrift Savings Plan (TSP) rule changes that took effect on January 1, 2026.

American Alternative Assets timed the release to Memorial Day — a national day of remembrance for those who gave their lives in military service — as part of the company's broader commitment to helping veterans, active-duty service members, federal employees, and their families make informed decisions about precious metals.

The guide consolidates American Alternative Assets' published research on the TSP into a single, plain-English resource and is available free at americanalternativeassets.com/blog/2026-tsp-diversification-guide.

Source: American Alternative Assets

VA’s EHR Rollout Gets Bipartisan Praise, but Issues Still Exist

The VA’s electronic health record (EHR) rollout is receiving bipartisan praise, but significant issues still remain, according to recent reporting.

Lawmakers from both parties say the resumed rollout appears to be “back on track,” especially after successful deployments at four Michigan VA medical centers in 2026. VA Secretary Doug Collins described the Michigan go lives as “phenomenal,” and demand from additional sites to join the rollout has increased.

However, employee groups and clinicians warn that persistent problems continue, including:

• The same system failures seen in earlier deployments, such as outages and functionality issues.

• Unresolved patient safety and usability concerns at the earliest rollout sites, which the VA says it still needs to “go back” and fix.

Cost and complexity also remain major challenges. The original $10B Cerner contract—now Oracle Health—has ballooned to an estimated $37B, and the VA paused deployments for years to address safety and performance issues before restarting in 2026.

Bottom line: The VA’s EHR modernization is earning bipartisan praise for recent progress, but technical problems, safety concerns, and legacy site failures still exist, and the project remains one of the most expensive and complex IT efforts in federal history.

Sources:

Federal News Network

NextGovSee less

Federal Employee Balancing Act: Pension Income and Market Investments

Federal employees who receive a pension (FERS or CSRS) often face a tricky balancing act: how to combine that guaranteed income with investments like the TSP, IRAs, or taxable accounts so their retirement income is stable, tax efficient, and able to grow. Here’s a clear, structured summary of how experts say federal workers can balance the two.

Federal employees can balance pension income and investments by treating the pension as a stable, bond like income source, then adjusting their investment mix—especially in the TSP—to manage risk, inflation, taxes, and long term growth. The goal is to use the pension to cover essential expenses while allowing investments to grow and provide flexibility. (This is general guidance, not personal financial advice.)

How Federal Employees Typically Balance Pension + Investments

1. Treat the Pension as a “Bond Substitute”

Many planners view a FERS or CSRS pension as similar to owning a large bond portfolio because it provides predictable monthly income.

• This often allows retirees to hold more stocks in their TSP or IRAs than someone without a pension.

• The pension reduces the need to take withdrawals during market downturns.

2. Cover Essential Expenses With Guaranteed Income

Experts recommend matching pension + Social Security to essential expenses like housing, food, and insurance.

• Investments then fund discretionary spending, travel, gifts, and inflation protection.

• This reduces stress during market volatility.

3. Use TSP Investments for Growth and Inflation Protection

Because pensions grow slowly (FERS COLA is often below inflation), investments must help keep up with rising costs. Common approaches:

• Maintain meaningful exposure to C Fund (S&P 500) and S Fund (small/mid cap) for long term growth.

• Use G Fund for stability and short term withdrawals.

• Use I Fund for international diversification.

4. Plan Withdrawals Strategically

Federal retirees often use:

• TSP withdrawals for early retirement years

• Social Security delay strategies to increase lifetime benefits

• Roth conversions in low tax years before RMDs begin

This helps smooth taxes and preserve flexibility.

5. Account for Survivor Benefits and Spousal Planning

Choosing a survivor benefit reduces pension income but protects a spouse. Investments can be used to offset the reduced pension or to provide additional survivor security.

6. Manage Taxes Across Multiple Income Streams

Federal retirees often juggle:

• Pension (taxable)

• TSP withdrawals (taxable)

• Roth accounts (tax free)

• Social Security (partially taxable)

Balancing these can reduce lifetime taxes—especially by planning withdrawals before age 73 RMDs.

Why This Balance Matters

A federal pension is powerful, but:

• It may not fully keep up with inflation

• It may not cover all expenses

• It ends or reduces at death without survivor benefits

Investments fill these gaps by providing growth, liquidity, and flexibility.

Sources:

Financial Content

GEBA.com

Markets.chronicaljournal.com

OPM.gov

What's New With The TSP Data Center.Com?

The biggest update to TSPDataCenter.com is that the entire site has been rebuilt and upgraded as of May 11, 2026, with major improvements to visuals, navigation, and data tools. The upgrade is significant enough that FedSmith published a full announcement about it.

⭐ The Most Important Changes

TSPDataCenter.com now functions like a modern financial dashboard, giving federal employees a clearer, faster way to track TSP performance.

1. Fully redesigned interface

Clean, professional layout

Optional dark mode

Faster navigation and updated visuals

2. Interactive charts for every TSP fund

Each fund (G, F, C, S, I, and all L Funds) now includes:

Price history charts with zoom controls (3 months → full history)

52‑week high/low visual indicator

Monthly returns heatmap (green = strong months, red = weak)

Annual returns bar chart

Rolling 1-, 3-, 5-, and 10‑year returns

“Best and worst months” lists

3. New homepage dashboard - You now see at a glance:

Current share prices

Daily, MTD, and YTD performance

YTD leaderboard

30‑day trend sparklines

4. New report sections for deeper analysis - These are built for serious TSP watchers:

Monthly Returns Quilt (full historical heatmap)

Annual Returns Report (multi‑fund comparison across all years)

Weekly Snapshot

Fund Comparison tools

📊 Latest TSP Fund Numbers (as of May 8, 2026)

From the live dashboard:

C Fund: +8.51% YTD

S Fund: +10.20% YTD

I Fund: +14.25% YTD

G Fund: +1.51% YTD

F Fund: +0.55% YTD

Sources:

FedSmith

TSPDataCenter.com

TSP Center

Costs & Trade‑offs of Suspending FEHB for Medicare Advantage Core Costs

Premium savings: Suspending FEHB stops your FEHB premium—often the biggest financial benefit for annuitants.

Higher risk of variable costs: Medicare Advantage (MA) plans can have low or $0 premiums, but out‑of‑pocket costs depend heavily on networks, referrals, and prior authorizations.

Main Trade‑offs

Provider access: FEHB + Medicare gives broad national access. MA plans restrict you to local networks and may charge more or deny out‑of‑network care.

Predictability: FEHB with Medicare as primary is usually more stable and predictable year to year. MA plans can change networks, benefits, and drug formularies annually.

Care management: MA uses more prior authorization and utilization controls than FEHB, which can delay or limit services.

Flexibility to return: You can return to FEHB during Open Season, but if you get sick mid‑year, you may be stuck in the MA plan until the next Open Season.

When MA may be cheaper

You’re healthy

You live in a county with strong MA plans

You prioritize lower premiums over maximum flexibility

When FEHB is usually safer

You have chronic conditions

You want national provider choice

You prefer predictable costs and fewer administrative hurdles

Sources:

Government Executive

FedSmith

Federal News Network

.

FERS Disability Retirement: Eligibility Requirements & Application Process

FERS Disability Retirement requires at least 18 months of FERS service, a medical condition lasting at least one year that prevents useful and efficient service, no available accommodation or reassignment, and a required Social Security disability application. The application must be filed before separation or within one year after.

Below is a concise, structured summary with sourced facts.

⭐ Eligibility Requirements (FERS)

Minimum service: At least 18 months of creditable civilian service under FERS.

Disabling medical condition: A disease or injury must make you unable to provide useful and efficient service in your current position.

Expected duration: The condition must be expected to last at least one year.

No accommodation or reassignment available: Your agency must certify it cannot accommodate your condition or reassign you to a vacant position at the same grade/pay within your commuting area.

Social Security Disability application (FERS only): You must apply for Social Security Disability Insurance (SSDI), even if you expect to be denied.

Timely filing: You must apply before separation or within one year after separation (strictly enforced except for documented mental incompetence).

📝 Application Process (High‑Level)

01

Confirm basic eligibility. Verify you have 18 months of FERS service and a medical condition expected to last at least one year.

02

Work with your agency. Your agency must attempt accommodation or reassignment and certify if neither is possible.

03

Gather medical documentation. Obtain physician statements and evidence showing you cannot perform essential job duties.

04

Complete OPM disability forms. Prepare the SF 3112 packet, including employee, supervisor, and medical provider sections.

05

Apply for Social Security Disability. Submit an SSDI application as required for all FERS disability applicants.

06

Submit your application to OPM. File before separation or within one year after; OPM reviews medical and agency evidence.

Sources:

My Federal Retirement

Legal Clarity

.

The Thrift Savings Plan (TSP) Saw a Strong Rebound in April 2026

April delivered one of the strongest monthly performances in recent years for TSP investors. After a volatile March, markets surged on easing geopolitical fears, strong corporate earnings (especially tech and AI), and renewed investor confidence.

Key April 2026 Returns

• C Fund (Large-cap stocks): +10.49% — one of the top five monthly gains ever for the fund.

• S Fund (Small/mid-cap stocks): +9.96% — boosted by broad “risk-on” sentiment.

• I Fund (International stocks): +9.11% — lifted by global recovery and tech spillover.

• G Fund: +0.36% — steady, low-risk growth as expected.

• F Fund: +0.12% — modest bond rebound after a weak March.

Lifecycle (L) Funds also rose across the board, with returns ranging from +2.95% (L Income) to +9.84% (L 2055–2075).

📈 Why TSP Funds Surged in April

FedSmith’s analysis highlights several drivers behind the rebound:

• Relief from geopolitical fears — markets priced in a crisis in March that did not materialize.

• Strong earnings, especially in tech and AI sectors.

• Solid economic data — not spectacular, but stable enough to support risk-taking.

• Investors rushing back into stocks after March’s selloff.

This combination produced unusually large single month gains — the kind typically seen over an entire year.

🧭 What This Means for TSP Participants

• April’s surge significantly improved year to date performance across stock funds.

• The C Fund remains the strongest performer, driven by large-cap tech.

• The G Fund continues to offer stability, but with much lower returns.

• Investors should remember that volatility cuts both ways — April’s gains followed a sharp downturn in March.

📌 Quick Comparison Table

TSP Fund April 2026 Return What Drove It

C Fund +10.49% Tech earnings, market relief

S Fund +9.96% Risk-on sentiment

I Fund +9.11% Global rebound, tech spillover

F Fund +0.12% Mild bond recovery

G Fund +0.36% Stable Treasury-based growth

Sources:

TSP Data Center

FedSmith

.

What are Federal Employees' FEHB, Medicare, and LTC Costs in Retirement?

Federal retirees rely on three separate systems—FEHB, Medicare, and long‑term care (LTC) solutions—and each covers a different part of retirement health costs. FEHB provides broad medical insurance, Medicare adds hospital and medical coverage at 65, and neither covers custodial long‑term care, which is why LTC costs must be planned for separately.

FEHB in Retirement

You can continue FEHB if you retire on an immediate annuity and were enrolled for the 5 years before retirement.

The government continues paying about 70–75% of premiums; retirees pay with after‑tax dollars.

FEHB provides comprehensive medical coverage but does not cover custodial long‑term care (inference based on FEHB program structure; not directly stated in sources).

Medicare at 65

Enrollment is optional for most federal retirees; Medicare becomes a decision point at age 65.

Part A: Hospital insurance, usually premium‑free.

Part B: Outpatient care; requires a monthly premium and may increase with income (IRMAA).

Part C (Advantage): Private plans combining A & B.

Part D: Prescription coverage (FEHB already includes drug coverage; inference that Part D is often unnecessary).

When enrolled in both FEHB + Medicare B, Medicare pays first, FEHB second, reducing out‑of‑pocket costs.

Postal retirees generally must enroll in Part B to keep PSHB coverage.

Long‑Term Care (LTC) Costs

Neither FEHB nor Medicare covers custodial long‑term care, such as assisted living, memory care, or long‑term home‑health aide support (inference based on Medicare’s limited skilled‑nursing coverage and FEHB’s medical‑only design).

Medicare only covers limited skilled nursing after a qualifying hospital stay.

LTC costs are significant (industry averages, not from sources):

Nursing home: ~$100,000+/year

Assisted living: ~$60,000/year

Home care: ~$30–80/hour

Quick Comparison

Program

What It Covers

Key Limits

FEHB

Medical, hospital, outpatient, prescriptions

No custodial LTC; premiums after‑tax in retirement

Medicare A

Hospital, limited skilled nursing

No custodial LTC

Medicare B

Outpatient, doctors, preventive

Premium required; no LTC

LTC Needs

—

Must be privately paid or insured; not covered by FEHB/Medicare

Sources:

Federal News Network

My Federal Retirement

OPM’s FY 2027 Budget Proposal

OPM’s 2027 budget proposal focuses on modernizing federal HR systems, expanding skills‑based hiring, and digitizing retirement and health benefits services, all while operating with a significantly reduced workforce and a lower funding request than previous years.

1. Total Funding Request

OPM requests $375 million in discretionary funding for FY 2027, which is lower than both current funding levels and the House’s proposed $418 million.

The reduced request reflects OPM’s effort to increase service delivery while decreasing operational costs.

2. Major Workforce Reductions

Since 2025, OPM has lost over one‑third of its workforce (more than 1,000 employees).

The 2027 budget supports approximately 2,074 full‑time equivalents (FTEs).

3. Core Priority: HR Modernization

OPM’s proposal centers on a government‑wide overhaul of federal HR systems:

a. Consolidating 100+ HR IT systems

OPM plans to replace more than 100 fragmented HR systems with a unified “Core HCM” platform integrating personnel processing, analytics, self‑service, and learning tools.

b. Expanding pooled recruitment & shared certificates

Multiple agencies will be able to hire from shared applicant pools, reducing duplication and speeding hiring.

c. Skills‑based hiring

OPM will continue shifting hiring away from degree requirements toward skills‑based assessments, including updated occupational families and expanded technical assessments.

4. Retirement Services Modernization

OPM proposes major upgrades to improve retiree services:

Digitizing retirement processing, expanding the Online Retirement Application to more case types.

Funding request: $147.1 million for Retirement Services.

Enhancements include a consolidated Digital File System, updated JANUS calculator, and improved call center automation.

5. Health Benefits System Improvements

For FEHB and PSHB programs, OPM proposes:

$1.2 million for the Carrier Connect platform.

$1.8 million for a decision‑support tool to help enrollees compare plans.

These upgrades aim to make health benefits enrollment more transparent and user‑friendly

6. Broader Strategic Goals

Across all initiatives, OPM emphasizes:

Attracting and retaining top talent

Delivering efficient, high‑quality service

Ensuring the federal workforce has the skills needed for a modern, tech‑driven economy

Sources:

Federal News Network

MSN

OPM

_________________________________________________________________________________________________________________

As federal employers, U.S. agencies are mandated by the U.S. Office of Personnel Management (OPM) to provide benefit training for their employees. This training should be provided by high-quality educators with not only significant knowledge of federal benefits but also insight into how to maximize those benefits in the context of the real world.

Carol Schmidlin, President of Franklin Planning has over 20 years of experience training federal agencies and their employees on how optimize their federal benefits and retirement planning. Carol provides high-impact and interactive workshops at your agency location or virtually via Zoom or Microsoft Teams.

We provide one- and two-day retirement FERS workshops pre-retirees, mid-career and FERS early career. Please contact us for a course agenda.

We also provide two complimentary one-hour programs per year called Knowledge Now, to inform and educate on specific topics related to federal benefits. These sessions are presented as a live webinar. Please contact for a list of topics.